Book Consultation

With the income tax situation changing, it is more crucial for firms to remain connected with their tax affairs. One of the major areas which partnership firms should be well aware of is Section 194T of the Income Tax Act, 1961 introduced in the Finance (No. 2) Bill, 2024, concerning the Tax Deducted at Source (TDS) on payment made to partners. This provision aims to ensure that tax compliance is streamlined and that partners are fairly taxed on the distributions they receive. In this blog, we’ll delve into Section 194T, exploring its implications for partnership firms and partners, and how it affects the broader landscape of income tax e-filing in India.

Section 194T was added to solve the issue of tax on payment given by partnership companies to their partners. According to this section, any payment in excess of a certain amount received by a partner from the partnership firm would be subject to TDS. The very fundamental concept of TDS itself is to check if the tax is being deducted at the time of generation of income so that potential evasion of tax might be avoided.

Section 194T would be particularly effective for:

It is compulsory for firms in partnership to monitor their payments so that this section is complied with, particularly as far as remitting their income tax returns is concerned. If the TDS is not deducted, then it will attract penalties and interest, and this will cause problems in the entire firm filing its taxes.

It is required to know the effect of TDS on partners in the interest of the firm and the partners. On payment made to partners, deducting TDS:

Compliance by the partnership firm and also by partners is mandatory under Section 194T provisions. Non-compliance can result in:

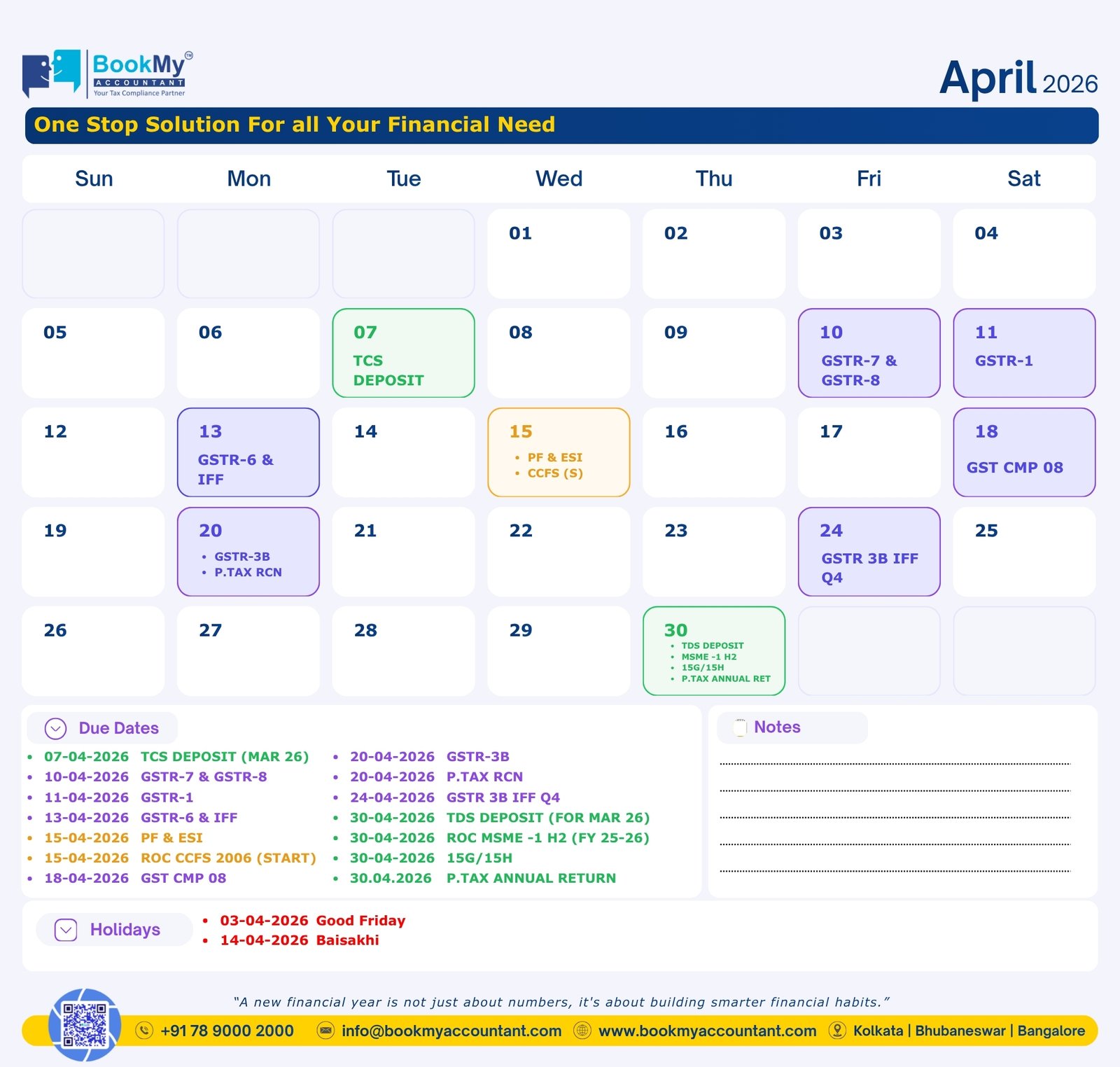

Process for filing taxes of partnership firms for TDS includes the following:

The Government of India has eased the process of e-filing income tax. Partnership firms and partners can now file their tax requirement online from the income tax e-filing portal. They are:

A successful tax planning largely depends on maintaining proper records. Partnership Firms should have proper records of:

This will not only become easy to file appropriately but will also ready the firm in advance for any potential demand from the income tax department.

| Type of Payment | TDS Applicability | Remarks |

| Salary/Remuneration | Yes | TDS applies if the aggregate exceeds ₹20,000 in a financial year. |

| Commission | Yes | TDS applies if the aggregate exceeds ₹20,000 in a financial year. |

| Bonus | Yes | TDS applies if the aggregate exceeds ₹20,000 in a financial year. |

| Interest on Capital/Loan | Yes | TDS applies if the aggregate exceeds ₹20,000 in a financial year. |

| Profit Share | No | Exempt from TDS under Section 194T. |

| Capital Withdrawal | No | Exempt from TDS under Section 194T. |

| Expense Reimbursement | No | Exempt from TDS under Section 194T. |

| ✅ Pros | ❌ Cons |

| Improved Tax Transparency Helps the Income Tax Department monitor partnership remuneration. | Cash Flow Disruption Partners may receive less than expected as TDS is cut upfront. |

| Better Financial Planning Regular deduction helps partners manage advance tax and avoid last-minute burdens. | Increased Compliance Burden More documentation, TDS returns, and deadlines to handle for firms. |

| Stronger Documentation & Accountability Firms are encouraged to maintain clear financial records, improving audit-readiness. | TDS on Book Entries TDS applies even on credited (not paid) amounts—affecting firms with cash constraints. |

| Ease in ITR Filing for Partners With TDS credit shown in Form 26AS, partners can smoothly proceed with income tax return filing. | Ambiguity in Deed Interpretation If the partnership deed isn’t clearly defined, categorizing payments becomes tricky. |

| Aligns with Digital India Mission Encourages usage of income tax e filing portal, and other paperless tools. | Risk of Penalties Delay in deduction, payment, or filing of TDS returns may lead to interest, penalty, or disallowance of expenses. |

Due to the intricacy in taxation and rules under Section 194T, it is recommended that partnership firms use tax experts or consultants. This assists businesses:

All the partnership firms in India need to be aware of Section 194T. With due precautions while being TDS compliant and making use of facilities available on the website of e-filing income tax, firms can manage their taxations better. Tax tides change constantly and hence it is better to remain updated so that partners and partnerships can both meet their dues and pay lesser tax.

Overall, Section 194T is not only a compliance but also a chance for partnership firms to enhance their financial health by adopting strategic tax planning. Having knowledge about the TDS mechanism and its impact on income tax return filing, partnerships can foster transparency cultures, sense of responsibility, and compliance that ultimately prove to be beneficial to all concerned stakeholders.

📌 Disclaimer by Book My Accountant (BMA):

This blog is for informational purposes only and does not constitute legal or tax advice. Readers are advised to consult their tax advisors or reach out to Book My Accountant (BMA) for tailored professional guidance based on their specific circumstances. BMA will not be liable for any decision taken based on the content of this blog.

"*" indicates required fields