Book Consultation

CCFS-2026 Late Fee Waiver is a major compliance relief scheme introduced by the Ministry of Corporate Affairs (MCA) for inactive and defaulting companies in India. The scheme allows eligible companies to save up to 90% on ROC late filing penalties, regularize pending filings, and avoid severe compliance consequences before the July 15, 2026 deadline.

Many people started companies as part of their entrepreneurial vision. But many of these visions were disrupted. Market trends shifted. Major funding difficulties arose. Internal partner disputes emerged. Other unexpected events occurred. These factors led to total or partial business shutdowns. When these businesses shut down, business owners found new businesses to operate but remained tied to the existing corporate structure.

This undesired neglect creates a significant, yet silent cost on the corporate promoter and the country.

Regulatory requirements from the Ministry of Corporate Affairs govern inactive companies. A company will never automatically shut down just because it is inactive. Instead, an inactive company continues to exist legally. It exists as long as it has not filed for bankruptcy. This remains true even when there are no sales. There may be no funds in the bank. There may be no employee payrolls. There may be no GST filings.

A common misconception among many directors is that, due to the inactivity of their business, it is unnecessary to file compliance forms since they will not have generated any revenue during its period of dormancy. This single belief tends to create very large financial problems. Under the current legal framework, statutory filing defaults will automatically incur an ongoing, unlimited, late filing penalty of ₹100 each day that a failure to file occurs for each form. This can add up over a period of complete dormancy. Promoters of inactive companies eventually receive notices to pay substantial penalties. These penalties have been accumulating over time. The notices arrive during unexpected or urgent times. For example, a promoter may need funds to raise new equity. They may need to secure bank loans. They may want to launch an unrelated new business venture. They may need to conduct corporate due diligence. Or they may need to liquidate the legal entity.

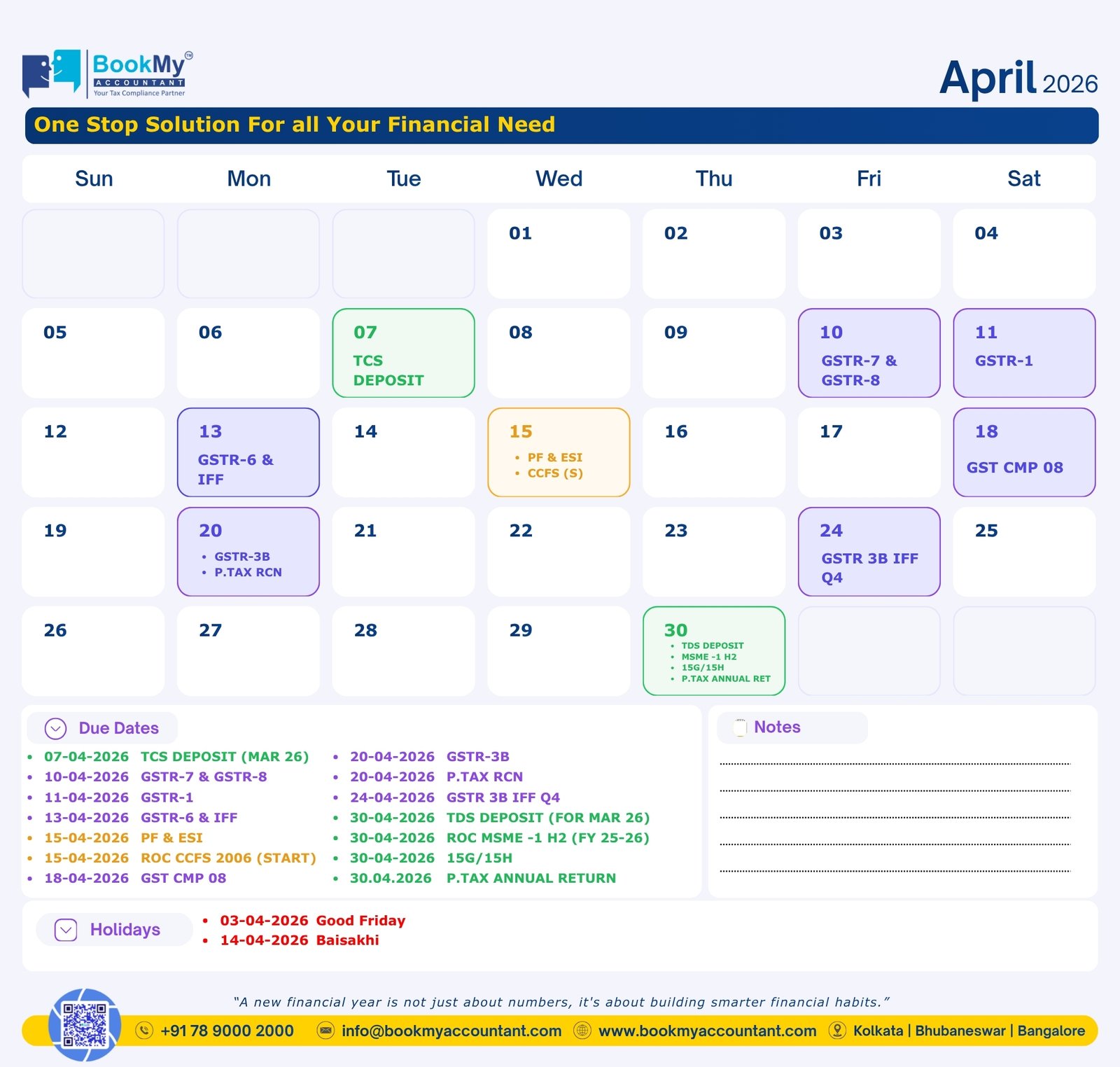

In order to find a solution for this nationwide problem, the Government of India has set up the Companies Compliance Facilitation Scheme 2026 (CCFS-2026) via MCA General Circular No. 01/2026. This amnesty scheme will run from April 15, 2026 to July 15, 2026 and is an unprecedented opportunity for companies that have not reported their compliance with ROC records to correct that compliance at a substantially reduced cost.

The catch is that not all companies are eligible for a clean slate. How your company will exit the CCFS will depend on whether or not your company meets the criteria outlined in the CCFS Negative List. If you do not qualify, you will be excluded from the CCFS, and you will be liable to face further legal liabilities and be subject to active prosecution for your actions.

CCFS-2026 is designed as an amnesty program specifically for corporations and to reduce excessive fees associated with malfeasance (failure to file). The MCA (Ministry of Corporate Affairs) has developed this financial program to assist small businesses and MSMEs (micro, small and medium-sized enterprises) through elimination of penalties accrued as a result of their failure to appropriately update their statutory records due to the high penalty rates.

In normal times, a business that fails to file the last three years of its annual returns will have with respect to accumulated late fees, likely in excess of ₹200,000 total. CCFS-2026 changes businesses’ financial situation by allowing them three different pathways to multiply the effect of their financial situation:

The Negative List is a key regulatory barrier to certain types of corporations claiming exemptions from fees. CCFS-2026 clearly defines the categories of companies that are not eligible for fee waivers, penalty relief, or immunity from prosecution.

Filing an MCA21 V3 application without checking eligibility under the Negative List can lead to immediate rejection. It may also result in loss of the filing fee and exposure to strict enforcement actions.

Companies that have already been struck off cannot benefit from CCFS-2026. The scheme is unavailable once the ROC initiates action under Section 248 for non-compliance.

If the ROC issues a final strike-off notice due to non-filing for three or more years, the company becomes ineligible for the amnesty window. In such cases, promoters must follow the lengthy restoration process before the NCLT.

The following benefits will not be available to businesses that have previously applied to strike themselves off or that previously been marked dormant. If either your business management previously attempted to strike off your business through e-filing Form STK-2 or through e-filing Form MSC-1 to obtain the dormant status prior to April 15, 2026, then you will not have the ability to claim any refunds or to process any application for the discounted fees retroactively.

In terms of corporate negligence, the "vanish category" represents the ultimate level/type of company failure. By definition from the regulators, this categorization describes companies that obtained public funding or credit and have completely abandoned all regulatory obligations. If your company has a registered office that does not physically exist, has no identifiable operations, and its registered directors cannot be found through conventional channels of communication and have effectively "vanished," it will be permanently listed on the "whitelist" or blacklist. Government will never allow an inexpensive amnesty offer to any untraceable management.

Entities that ceased to exist due to mergers, restructurings, or court-approved amalgamations are not covered under this framework. Their corporate history already forms part of the surviving entity. Therefore, they are no longer treated as independent legal entities eligible for a fresh compliance status.

• CCFS-2026 assists legitimate, struggling owners in catching up on real delays — not in helping bad actors escape.

This system exclusively prohibits companies who are currently under an active investigation, fraud inquiry, or structural enforcement action undertaken by:

- The Serious Fraud Investigation Office (SFIO)

- The Enforcement Directorate (ED)

- The Income Tax Department or the Central Board of Direct Taxes (CBDT)

- State and Regional anti-fraud, corporate scan departments

• Companies involved in fake GST billing, tax evasion, money laundering, accommodation entries, or shell company activities will remain on the Negative List. Investigating agencies will strictly monitor such entities.

CCFS-2026 immunity solely applies, therefore, to the penalties or prosecution for trespass that arise directly from the default of statutory returns. In fine: No protection under law, no corporate immunity, no pardon in respect of corporate fraud, and no exemption in respect of accounting falsification, tax evasion, or any criminal liabilities.

This unprecedented three-month corporate reset fully removes thousands of companies from the Negative List.

Many entrepreneurs incorporated their privately held companies over the last several economic cycles and have encountered operational walls before getting to the stage of scale-up; for these business owners to qualify for future funding from venture capital firms and to be able to conduct business again through their retained/inactive company(s), the CCFS-2026 provides the opportunity for owners who have an inactive entity with significant compliance issues to regularize their previous complete filing history through the payment of a small fee.

Most family-run businesses created multi-tiered, multi-business corporate divisions that added new lines, but the family later abandoned or failed to develop them. Families can take advantage of this opportunity by removing their already existing debt related to the corporation's previous business model and therefore establishing a strong, low-cost process to close their corporation in a safe manner.

According to Section 164 of the Act, if any company fails to submit their financial statements and/or annual returns to the Registrar of Companies for a continuous period of three financial years, then the company's directors shall immediately become ineligible for a period of five years. A direct result of being disqualified is that the director will automatically lose his/her Director Identification Number (DIN). The use of this eligibility disqualification can provide a powerful source of protection to a director (by allowing them to obtain a new DIN) if the company has outstanding financial statements/annual return filings.

Companies with pending annual filings and heavy late fees can benefit from the CCFS-2026 window. The scheme allows businesses to clear various long-pending annual and event-based compliance forms.

To navigate the MCA21 V3 portal successfully during an amnesty window (which provides an opportunity for companies to clear any non-compliance issues in a timely manner) takes a high degree of operational accuracy. BMA is your trusted partner, providing you with corporate growth and organization structure alignment for your entire package of documentation to pass through all the regulatory screening processes without any issues.

BMA does not rely on guesswork; we log directly into your master dashboard on the official MCA Portal to conduct a structural compliance audit of ten going back to every unfiled form that dates from a previous financial cycle. We develop a real-time report showing the total amount of fees you are entitled to receive in reducing the total fees you have incurred, and provide this information prior to your uploading any documents.

2. Financial Reconstruction and Statutory Auditing

Financial reconstruction and statutory auditing cannot be accomplished utilizing a blank or hypothetical informational template as part of the standard registration process. Each missing yearly record of compliance will be reconstructed by BMA’s firm of accountants in order to provide annual balance sheets in retrospect for any year not complying with the Financial Care Regulations. Director’s Reports will be established outlining BMA’s firm of accountants are the only independently registered and certified accountants to sign off/ validate a Form AOC-4 Data Package.

3. Aligned Auditor Mandate Prioritization

Processing financial statements through the V3 system architecture has been a significant example of a structural bottleneck due to not having an active verified auditor associated with your Corporate Identification Number (CIN) to develop financial statements. BMA is responsible for preparing and submitting the overdue Form ADT-1 for your company as a priority and fixing all backend system-generated errors associated with your financial statements to ensure they flow smoothly through the system.

4. Managing DSCs and Uploads to Portals

We will audit and verify your management group Director Identification Number (DIN) and update your mandatory DIR-3 KYC filings, so that all directors will have an active status. Our processing team will prepare and coordinate all Digital Crypto Signatures (DSCs) and explicitly complete your data forms according to the CCFS-2026 prompt, ensuring you receive an automatic 90% penalty reduction at payment processing.

Management teams have to be careful not to trip into operational pitfalls as compliance teams go quickly towards the upcoming summer deadline.

1. Believing in the "No Business" Myth:

Simply repeating “no operations” will not stop an automated MCA compliance algorithm from applying hefty penalties against your company's financial resources. The law imposes an indiscriminate obligation to file until a firm has been removed from the franchise register.

2. Expecting a Last-minute System Extension:

There have historically been founders waiting to file again so they could receive an arbitrary extension from MCA to file with amnesty. The government has repeatedly sent very clear messages that there is a firm no-extension date of July 15th, 2026.

3. Filing Documents Without a Complete Negative List:

Filing non-compliant forms with the intention of being difficult with the system will result in the loss of all the filing fees for any entity in consideration of the drawing of increased government scrutiny attached directly through the governing body.

Procrastination when it comes to adhering to compliance regulations is one of the top reasons for companies’ failure to generate any revenue after they close their doors.

Companies can no longer let an inactive company sit idle for years while ignoring compliance requirements to the fullest extent of the law — this old theory is no longer practical in the heavily regulated and electronically monitored climate of India. After the cut-off date of July 15, 2026, the imposition of penalties from the regular penalty regime will recommence on a daily basis at ₹100 per day per form.

The Ministry of Corporate Affairs (MCA) is likely to institute severe penalties under 454 against all defunct corporate entities whose directors have been ignoring compliance requirements for years. The penalties could be significant and may include monetary penalties against the directors and corporate entities as well as movement to the Negative List.

As such, the CCFS-2026 implementation framework provides your company with the best opportunity to reduce potential penalties under the "normal" regime by up to 90%, to create a plan that eliminates any previous non-compliance issues associated with earlier years, and to create a successful exit for your company and a legal exit from the Negative List. Reach out to the compliance team at BMA today for assistance with preparing for compliance with the CCFS-2026 implementation framework and with addressing negative list compliance for your company.

"*" indicates required fields