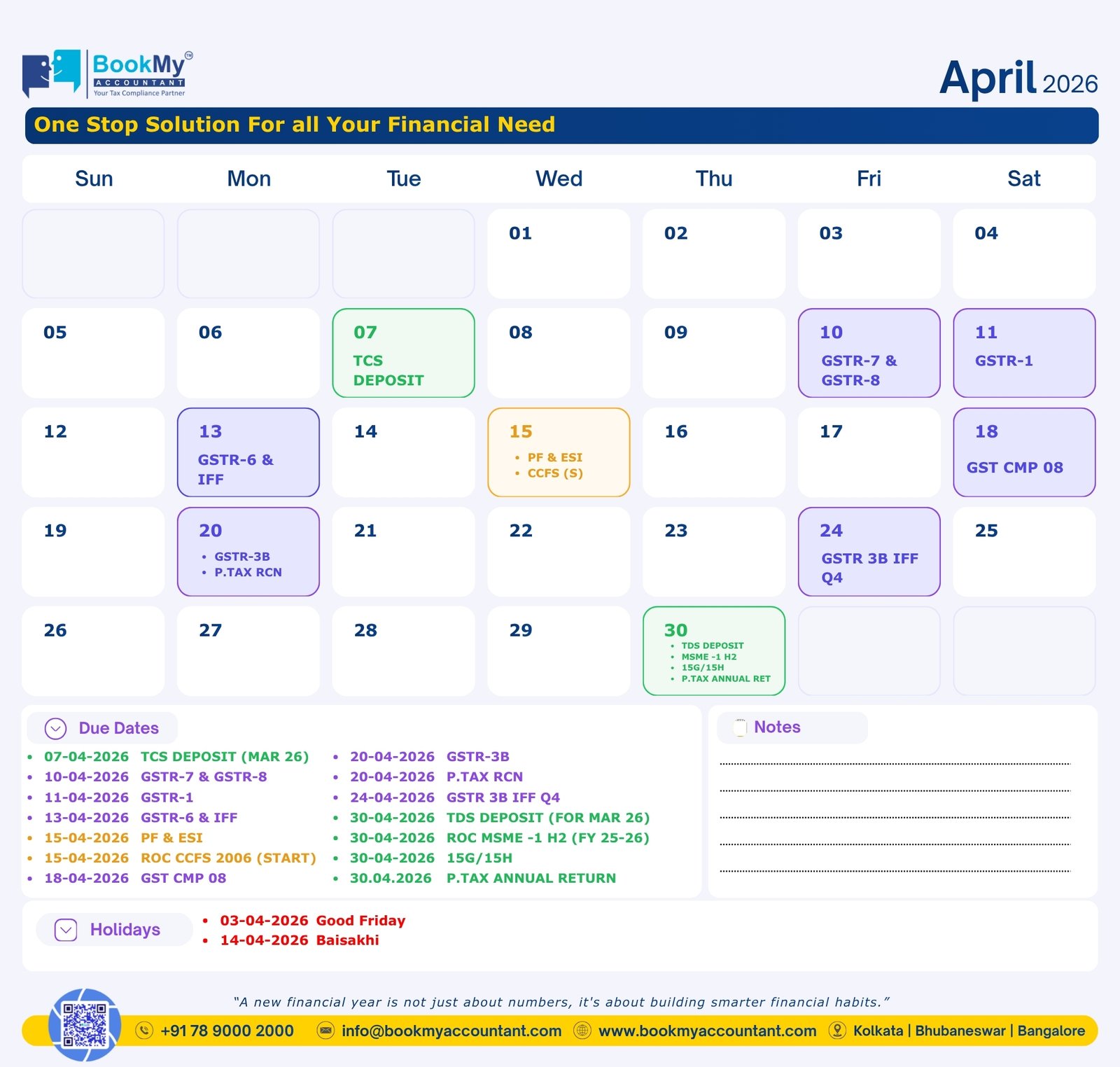

Book Consultation

The UPI Revolution and Its Position in Contemporary Financial Life

Unified Payments Interface (UPI) has revolutionized India's way of paying. A swift QR code scan or tap of the button, and one is done with payments in mere seconds—be it the ride, grocery shopping, or even the roadside tea. It has done away with the inconveniences of cash or card swipes to facilitate quick and convenient payments even for the most fundamental financial transactions.

UPI is being touted as the most successful live payment system in the world. Yet, although unmatched in convenience, its growing popularity has raised genuine raised eyebrows of taxpayers, small merchants, and businessmen alike regarding transparency, record-keeping, and compliance.

Is UPI, then, a digital blessing or an invisible financial bane?

Let us weigh both sides.

One of the biggest strengths of UPI is its digital trail left behind. Each transaction is timestamped, recorded, and made available through user-friendly applications such as Google Pay, PhonePe, BHIM, Paytm, and others.

This can prove to be of immense benefit in the following manner:

1. Better Taxation Filing and Planning of Budget

UPI transactions also leave behind a transparent, organized record of incomes and expenses. For individuals, freelancers, and entrepreneurs, this makes tax preparation and accuracy easier. No more scrambling through receipts—just glance at your app statement.

2. Reduced Utilization of Unaccounted Cash

India has been extremely cash-oriented historically. UPI has helped reduce cash dependence, hence formalizing greater components of the economy. This translates into better tax compliance and accountability.

3. Broader Financial Inclusion

According to AU Bank, UPI has enabled people who previously had no access to formal banking systems to take advantage of the digital economy. Rural shopkeepers, rural wage workers, and micro-vendors are able to receive payments effortlessly and at no expense without expensive POS machines.

4. Enhanced Creditworthiness

A clean and timely history of digital payments enhances an individual's credit profile. This opens the door to availing loans, subsidies, and business loans easily.

While it has its advantages, UPI also has its drawbacks—particularly for the ignorant about its tax and compliances implications.

1. Paying More through Impeccable Payments

India Today indicated that almost 75% of UPI users confess to increasing expenditure. Since there is no actual cash transfer, individuals lose track of the amount spent.

It is this "hidden spending" that is the problem when

2. Unintended Tax Implications on Small Vendors

Picture this: a roadside tea seller now takes UPI. Within a year, their cumulative digital payments exceed ₹20 lakhs. Even if the margin is slim, now the number of transactions attracts investigation by tax bodies or even GST registration levels.

This has been the reason for the UPI usage decline in some small business communities in states such as Karnataka. The merchants feel penalized for embracing digital behavior as tax regulations are ambiguous.

3. Ambiguity Over UPI Income Rules

In most instances, professional and business dealings are grouped in one UPI ID. This commingles taxable income and informal payments (such as reimbursement from buddies).

If taxpayers don't classify it correctly, auditors often flag even non-taxable revenue—wasting time, money, and effort.

| Benefits | Pitfalls |

| Makes Transactions Transparent – All transactions are traced and documented | Promotes Expenditure Without Means – Ease makes impulse buying more likely |

| Reduces Black Money Flow – Encourages cleaner, compliant transactions | Generates Tax Nerves among Traders – Unnecessary digital volumes without context may draw inquisitive questions |

| Enhances Credit Availability – UPI history creates a financial history | No Segregation – Blending business and personal UPI payments generates confusion |

| Makes Correct Filing of ITR Easy – Easy to track and report income and outgoings | Misrepresentation of Payments – Non-taxable funds may be reported as taxable income |

| Supports Financial Planning – Simple to view past history from UPI statements | No Framework Defined Yet – Lack of standardized taxation policy on UPI usage |

As a regular user of UPI for personal and business spendings, here is how you can remain compliant and worry-free:

1. Keep Your UPI Transaction History in Check

Avail monthly UPI statements through your app or bank. This serves the purpose of:

2. Use a Different UPI IDs for Business and Personal Transactions

Vendors, gig economy workers, and freelance workers must never combine personal expenditures and business receipts. It helps you to file taxes methodically and guards you during audit.

3. Save Digital Records

Download and save monthly UPI statements at all times, particularly if you are reporting business or professional income. These can come in handy during audits or when seeking loans.

4. Assign UPI Spending Limits

PhonePe and Google Pay apps provide the facility to limit transactions. This easy step can prevent excessive spending and help you maintain a budget.

To implement UPI successfully without causing confusion or fear, the government must focus on the following measures:

How Book My Accountant (BMA) Can Help You

In Book My Accountant (BMA), we realize the increasing complexities of digital payments. You are an employee, freelancer, founder of a startup, or small trader, we provide tailored assistance to guide you through:

UPI is not just a payment system. It's a reflection of how well we're disciplined when it comes to money. If used intelligently, it can usher in unprecedented ease and transparency into our finances. But if you're unaware of it or misuse it, it can be a pain for money—particularly when it comes to taxes.

Do not wait for a notice or fine. Take control of your digital cash. With BMA's expert guidance, UPI can be a growth driver, not a stress factor.

UPI has revolutionized India's finance—convenience in payments, speed, and transparency. But higher convenience requires higher awareness.

Learn where UPI has a place in your tax life. Employ it as a smart money tool—not a trap. With professional advice from BMA, you can be treated by UPI without losing out on compliances.

The facts stated in this article are for general information purposes only and are not professional financial or legal advice. Book My Accountant (BMA) has attempted its best to state accurate information; however, we disclaim all responsibility for loss or inconvenience arising due to reliance on the content. You are advised to seek professional advice from a qualified tax consultant on an individual basis.

"*" indicates required fields